Maintaining the Chart of Accounts

Modern accounting systems offer tools for automating data entry, generating reports, and even suggesting account categorizations based on transaction types. Ensure your COA aligns with applicable accounting standards and legal requirements. Finally, regularly review and adjust your COA to reflect any changes in your business operations or financial reporting requirements. This ongoing adjustment ensures that your COA remains relevant and effective.

Unique identification

- Assigning numbers to accounts is a thoughtful process, designed to accommodate future expansions by reserving gaps for new accounts as the business grows or diversifies.

- Make sure that your line items have titles that make sense to you and your accountant, so use straightforward titles like ‘bank fees’, or ‘bottling equipment’.

- This method significantly mitigates the risk of errors and fraud, reinforcing the reliability of the financial data.

- It helps to categorize all transactions, working as a simple, at-a-glance reference point.

- This list includes every category under which you can classify money spent or earned by your business, from the salaries paid to employees to the revenue from sales.

Ensure that everyone involved in financial management and bookkeeping understands the account titles and uses them correctly, which will help maintain the integrity of your financial data. This categorization goes beyond merely adhering to accounting standards; it aligns with your business’s operational needs. For example, manufacturing businesses may require detailed accounts for inventory and cost of goods sold, whereas service-based businesses might prioritize expense accounts related to service delivery. For example, if a company makes a sale, it debits an asset account (like Accounts Receivable or Cash) and credits a revenue account (Sales Revenue), as defined in the COA. The company records each transaction (journal entry or accounting entry) in the general ledger account, and the general ledger totals create the trial balances.

What does COA stand for?

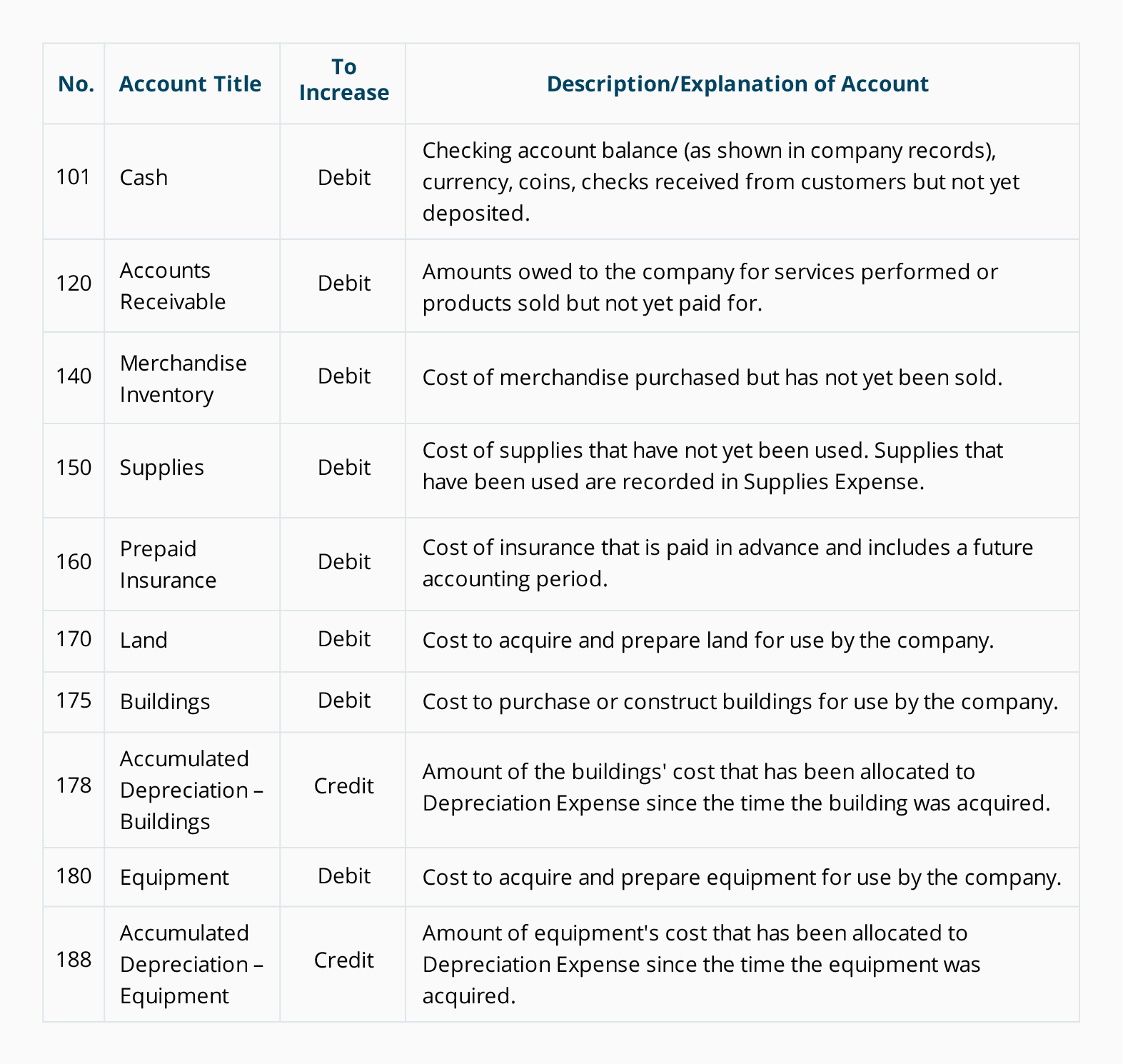

For example, bank fees and rent expenses might be account names you use. Accounting systems have a general ledger where you record your accounts to help balance your books. Keeping your accounts in place and up-to-date is important for analyzing your finances. COAs are typically made up of five main accounts, with each having multiple subaccounts. The average small business shouldn’t have to exceed this limit if its accounts are set up efficiently. However, they also must respect the guidelines set out by the Financial Accounting Standards Board (FASB) and generally accepted accounting principles (GAAP).

How to Set up a Chart of Accounts

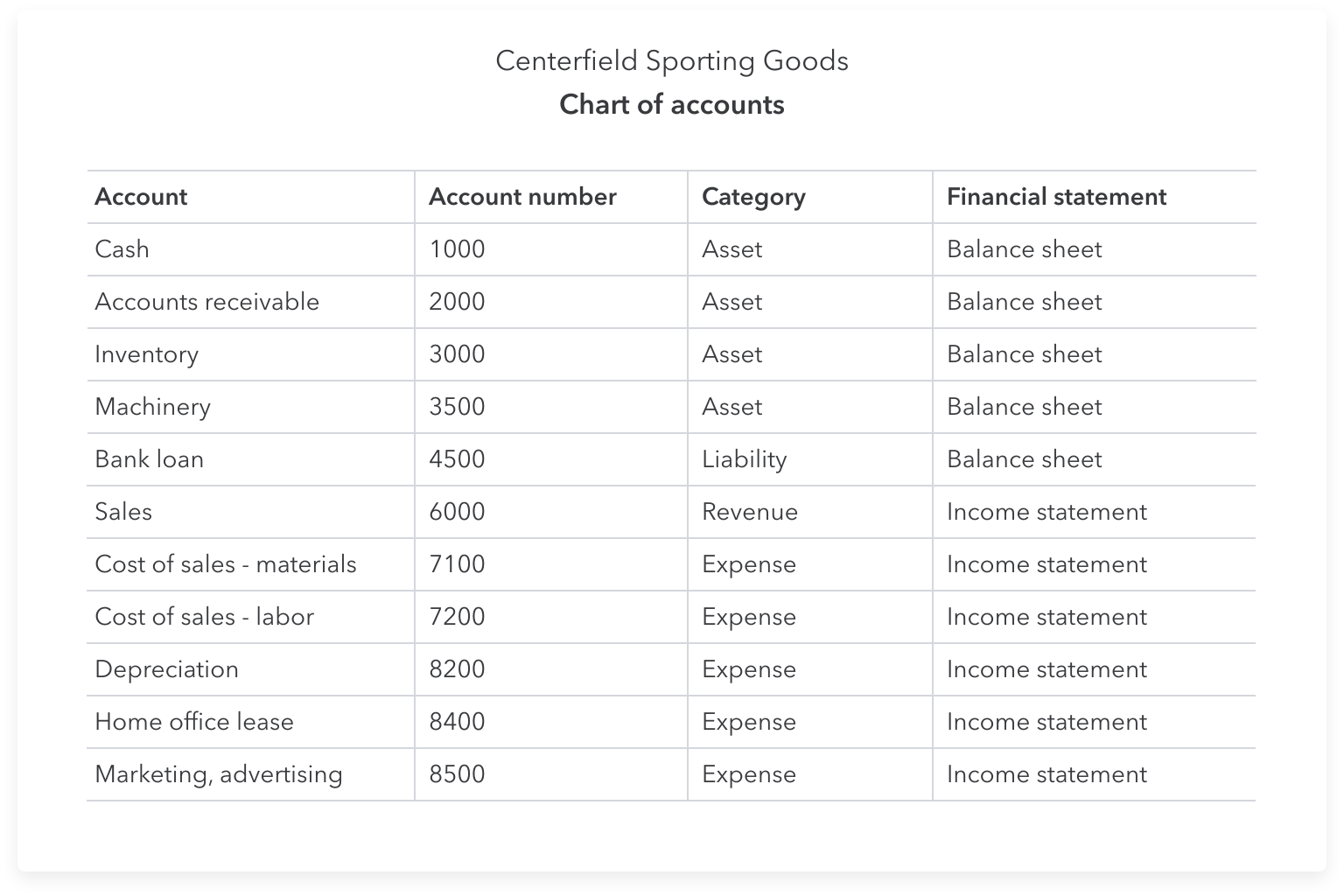

The remaining revenue and expenses accounts fall into the profit and loss accounts, as they appear in this financial statement. FreshBooks will help you stay organized with a user-friendly interface that keeps things simple. A chart of accounts is a document that numbers and lists all the financial transactions that a company conducts in an accounting period. The information is usually arranged in categories that match those on the balance sheet and income statement.

How a chart of accounts benefits your small business

The authorized user then implements the change in the development system and loads it in an open transport. Within the numbering system you’ve chosen, assign numbers to each account. Start with broader categories at the beginning of the range and get more specific as you move up. Long-term liabilities are financial obligations that are due after more than one year.

Can a chart of accounts be customized to fit specific business needs?

Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others. Our goal is to deliver the most understandable and comprehensive explanations of financial topics using simple writing complemented by helpful graphics and animation videos. We follow strict ethical what are the best invoice payment terms for your small business journalism practices, which includes presenting unbiased information and citing reliable, attributed resources. This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible. At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content.

We believe everyone should be able to make financial decisions with confidence. But experience has shown that the most common format organizes information by individual account and assigns each account a code and description. What’s important is to use the same format over time for the consistency of period-to-period and year-to-year comparisons.

An asset would have the prefix of 1 and an expense would have a prefix of 5. This structure can avoid confusion in the bookkeeper process and ensure the proper account is selected when recording transactions. Begin by thoroughly assessing your business model, size, industry, and specific financial transactions. This assessment will help tailor the COA to accurately reflect how your business operates financially. Consider the types of transactions you frequently handle, such as sales, purchases, payroll, and loans. Also, think about future business expansions or diversifications and how they might impact your accounting needs.

Some businesses can indicate COGS, gain and losses, etc., as separate accounts to structurize their finances even more granuarly. Just remember that while you can add an account to the chart at any time throughout the financial year, you should not delete any accounts until the end of an accounting period. Therefore, it is advisable to initially create a list of accounts that is unlikely to significantly change for as long as possible and keep it congruent among all areas of business.

Also consider any security measures needed to protect sensitive financial information stored in the system. Later on, regularly review and update your COA to reflect changes in your business operations, industry standards, or regulatory requirements. This may involve adding new accounts, removing obsolete ones, or reclassifying existing accounts to better suit your business’s evolving needs. Incorporate your newly created COA into your accounting software or manual accounting system. This might involve setting up each account within the software and ensuring that it aligns with your COA structure.

In the interest of not messing up your books, it’s best to wait until the end of the year to delete old accounts. An expense account balance, for example, shows how much money has been spent to operate your business, whereas a liabilities account balance shows how much money your business still owes. Doing so ensures that accurate comparisons of the company’s finances can be made over time.